Synopsis

What readers will learn by reading this article

-

Assess Financial Situation

How to assess their current financial situation, including income, expenses, debts, and assets.

-

Creating Comprehensive Budget

How to create a comprehensive budget aligned with their financial goals.

-

Financial Planning

How to manage debt, build an emergency fund, save & invest, understand taxes, plan for retirement, protect their financial future, and continually educate themselves in personal finance.

What is Personal Finance?

Before mastering, first let us understand, what is Personal Finance? Personal finance is a crucial aspect of our lives that often goes overlooked. It involves managing our financial resources, making informed decisions, and planning for the future. Mastering this art is not only about meeting our current financial needs but also about setting ourselves up for long-term financial stability and success. In this comprehensive guide, we will explore various areas of Powerful Personal Finance Strategies and provide practical tips to help you take control of your financial future.

| Aspect | Steps to Take |

|---|---|

| Income | – Calculate your total income |

| – Include all sources of income, such as salary, side hustle income, or investment returns | |

| Expenses | – Track your expenses |

| – Categorize expenses into fixed and variable expenses | |

| Debts | – Identify all types of debts you have |

| – Prioritize high-interest debts | |

| Assets | – Calculate your net worth |

| – Subtract your liabilities from your assets |

Reasoning: Assessing your personal financial situation is the first step towards mastering personal finance. By understanding your income, expenses, debts, and assets, you can make informed decisions and set realistic goals. Calculating understanding your cash flow are critical aspects of assessing your financial health.

Review the below video to understand your current financial situation and the personal finance aspects along with examples. There is a free Personal Finance Tracker included to get everyone acquainted with the Budgeting and tracking the goals.

The Importance of Personal Finance

Personal finance is about meeting and isn’t just about numbers, it’s the roadmap to achieving your dreams. Whether you’re aiming to cover those unexpected short-term expenses, embark on a well-deserved retirement, or set aside funds for your child’s college education, personal finance molds your aspirations into reality. It’s a fusion of income management, prudent spending, smart saving, savvy investing, and the security blanket of personal protection through insurance and estate planning.

Not having a firm grasp on financial management or lacking the discipline to navigate the financial landscape has left many people across the globe grappling with staggering debt.

To put it in perspective,

By Q2 2023, US Total Consumer Debt stands at 16.84 Trillion Dollar which is 4.5% higher than 2022 data.

By March 2023, India Total Household Deb stands at 486.7 Billion US Dollar.

Let’s break it down:

In US,

- Credit Cards Debt outstanding is at 1.02 Trillion which soared at 16.3% when compared to 2022.

- Auto loans stands at 1.50 Trillion. Up by 5.8% compared with 2022.

- The numbers tell a story of their own, one that highlights the critical importance of personal financial literacy and discipline in navigating the treacherous waters of modern finance.

In India,

- The “Net Financial Savings” of an average Indian Household hit a 47-year low in FY-2023.

- The net financial savings of an Indian households, which includes bank deposits, stocks, bonds and insurance policies, dropped to ₹13.8 trillion in 2022-23.

- Credit Card Spending in India has hit the ₹1 Lakh Crore mark. It’s actually a historic high of ₹1.48 lakh crore in August, 2023.

Areas of Personal Finance

Budgeting

| Step | Tips and Strategies |

|---|---|

| List income sources | – Include all sources of income, including salary, side hustle income, or investment returns |

| Track expenses | – Categorize expenses into fixed and variable expenses |

| Analyze spending | – Identify areas where you can cut back and save |

| Use appropriate tools | – Consider using budgeting apps or spreadsheets |

| – Automate your contributions and track your progress |

Reasoning: Creating a budget is a fundamental aspect of personal finance. It helps you allocate your income effectively, track your expenses, and identify areas where you can save money. Using appropriate tools and apps can simplify the process and provide insights into your spending patterns.

Managing debt

| Type of Debt | Strategies |

|---|---|

| High-interest debt | – Prioritize repayment of high-interest debts |

| – Consider debt avalanche or debt snowball method | |

| Debt consolidation | – Explore options for consolidating multiple debts |

| – Aim for lower interest rates |

Reasoning: Debt can be a significant burden on personal finances. Managing and eliminating debt should be a priority. High-interest debts should be tackled first, and strategies like the debt avalanche or debt snowball method can be used. Debt consolidation is another option to explore, as it can simplify repayment and potentially reduce overall interest payments.

Building an emergency fund

| Step | Tips and Strategies |

|---|---|

| Set a savings goal | – Aim for three to six months of living expenses |

| Establish a savings plan | – Automate your contributions |

| Prioritize saving | – Make saving a priority |

Reasoning: Building an emergency fund is crucial to handle unexpected expenses. Setting a savings goal and establishing a monthly savings plan can help you gradually build your fund needed during emergency. Making saving a priority ensures that you allocate a portion of your income towards this important goal.

Saving and investing

| Step | Tips and Strategies |

|---|---|

| Set SMART financial goals | – Consider short-term and long-term objectives |

| Educate yourself on investment options | – Understand stocks, bonds, mutual funds, and real estate |

| Consult with a financial consultant | – Seek professional guidance if needed |

Reasoning: Save the earnings and investing the money are essential for achieving financial goals and building wealth. Setting specific, measurable, achievable, relevant, and time-bound (SMART) goals provides clarity and motivation. Educating yourself about different investment options and consulting with a financial consultant can help you make informed investment decisions.

Understanding taxes

| Aspect | Tips and Strategies |

|---|---|

| Understand income tax | – Learn about tax brackets and sources of income |

| Maximize deductions | – Research and take advantage of available deductions and credits |

| Stay informed | – Stay updated on changes in tax laws |

Reasoning: Understanding taxes is crucial for effective personal finance management. It’s important to understand how different sources of income are taxed and how to maximize deductions and credits. Staying informed about changes in tax laws can help you make strategic financial decisions.

Planning for retirement

| Step | Tips and Strategies |

|---|---|

| Explore retirement savings options | – Consider 401(k) plans, Individual Retirement Accounts (IRAs), PPF, NPS etc in your respective country. |

| Determine the appropriate contribution amount | – Utilize retirement calculators to estimate savings goals |

| Consult with a financial advisor | – Seek professional guidance for retirement planning |

Reasoning: Planning for retirement is an important aspect of personal finance. Exploring different retirement savingsoptions and determining the appropriate contribution amount based on your goals is crucial. Consulting with a financial advisor or utilizing online retirement calculators can help you make informed decisions.

Protecting your financial future

| Aspect | Tips and Strategies |

|---|---|

| Health insurance | – Obtain health insurance coverage |

| Life insurance | – Consider life insurance if you have dependents |

| Property insurance | – Review and update insurance policies regularly |

| Estate planning | – Create a will. |

Reasoning: Protecting your financial future involves mitigating risks and ensuring financial security for you and your loved ones. Having health insurance, life insurance, and property insurance safeguards your assets. Estate planning ensures that your assets are distributed according to your wishes and minimizes conflicts among beneficiaries.

Continual education and improvement

| Aspect | Tips and Strategies |

|---|---|

| Books, podcasts, and courses | – Utilize various resources for financial education |

| Attend workshops or seminars | – Participate in financial literacy programs |

Reasoning: This is an important personal finance and most of us wouldn’t like to touch or explore. Personal Finance matters as it continues to evolve. It is important to learn and staying updated on the personal finance news, latest trends, strategies, and investment opportunities is essential for making informed financial decisions. Fortunately, there are numerous resources available to help you expand your financial literacy and improve your financial management skills.

Books, podcasts, and online courses are valuable tools for learning about personal finance. Many experts in the field share their knowledge and insights through these mediums, making complex financial concepts accessible to a wider audience. Take the time to explore different resources and find those that resonate with you and your learning style.

Attending financial literacy workshops or seminars can also provide valuable insights and networking opportunities. Many organizations, including banks and community centers, offer free or low-cost financial education programs. These events often cover a wide range of topics, from basic finance management to advanced investment strategies.

Assessing your financial situation

Before diving into the world of personal finance, it’s essential to assess your current financial situation. This involves evaluating and analyzing various aspects, including your income, expenses, debts, and assets. By understanding where you stand financially, you can make informed decisions and set realistic goals.

One crucial step in assessing your financial situation is calculating your Net Worth. It is the difference between your assets (such as cash, investments, and property) and your liabilities (such as loans, debt, and mortgages). Calculating your net worth gives you a clear picture of your overall financial health and helps you track your progress over time.

Understanding your cash flow is also vital. Cash flow refers to the money coming in and going out of your accounts. By tracking your income and expenses, you can identify areas where you might be overspending and find ways to optimize your finance management techniques.

Key Takeaway

Managing personal finance may require effort and discipline, but the benefits are well worth it. With these money tips in mind, you can take control of your financial future and work towards achieving your financial independence. Remember that personal financial management is an ongoing process, and small, consistent steps can lead to significant financial stability over time.

Personal Financial Strategies

Personal financial management, or managing your personal finance, is a critical skill that can significantly impact your financial well-being. It involves managing your money effectively to achieve financial stability and meet your financial dreams and goals. Whether you are just starting on your financial journey or looking to improve your money management skills, these money tips can help you manage your personal finance more effectively.

Devise Your Budget

A budget acts as your financial roadmap, guiding you towards your goals and helping you make informed spending decisions. It allows you to allocate your income effectively, track your expenses, and identify areas where you can save money.

To create a comprehensive budget, start by listing all your sources of income. This includes your salary, side hustle income, passive income or any other funds you receive regularly. Next, track your expenses by categorizing them into fixed expenses (such as rent, utilities, and loan payments) and variable expenses (such as groceries, dining out, and entertainment). Having a clear overview of your expenses will help you identify areas where you can cut back and save.

Using appropriate tools and apps can simplify the process and provide insights into your spending patterns. Many apps allow you to link your bank accounts and cards, automatically categorizing your expenses and generating reports. This makes it easier to track your progress and stay on top of your budget.

Limit and Reduce Debit

Debt can be a significant burden on your financial plan, making it essential to develop a strategy to manage and ultimately eliminate it. Start by understanding the different types of debt you have as a borrower, such as credit card debt, student loans, or a mortgage. Each type of debt may require a different approach.

High-interest debts, such as credit card debt, should be a priority when it comes to repayment. Paying off debt as quickly as possible can save you a significant amount of money in interest charges. Consider implementing the debt avalanche or debt snowball method to tackle your debts systematically.

Debt consolidation is another option to explore. This involves combining multiple debts into a single loan or card with a lower interest rate. Debt consolidation can simplify your pay back process and potentially reduce the overall interest you pay.

Establish an emergency

Life is full of unexpected events, and having a fund helps during crisis is crucial to handle these situations. This is a separate savings account specifically dedicated to covering unexpected expenses, such as medical bills/emergency, job loss, or even car repairs.

Building a Safety net to face crisis takes time and discipline. Start by setting a realistic savings goal, such as three to six months worth of living expenses. Then, establish a monthly savings plan and automate your contributions. By making saving a priority, you’ll gradually build your fund required during emergency and have peace of mind knowing that you’re prepared for any financial curveballs life throws your way.

Financial Plan

Saving and investing are essential components which will promote yourself as a best Financial Planner. Saving involves setting money aside for short-term goals or emergencies, while investing focuses on long-term growth and wealth accumulation. Both strategies play a crucial role in achieving financial freedom and building wealth over time.

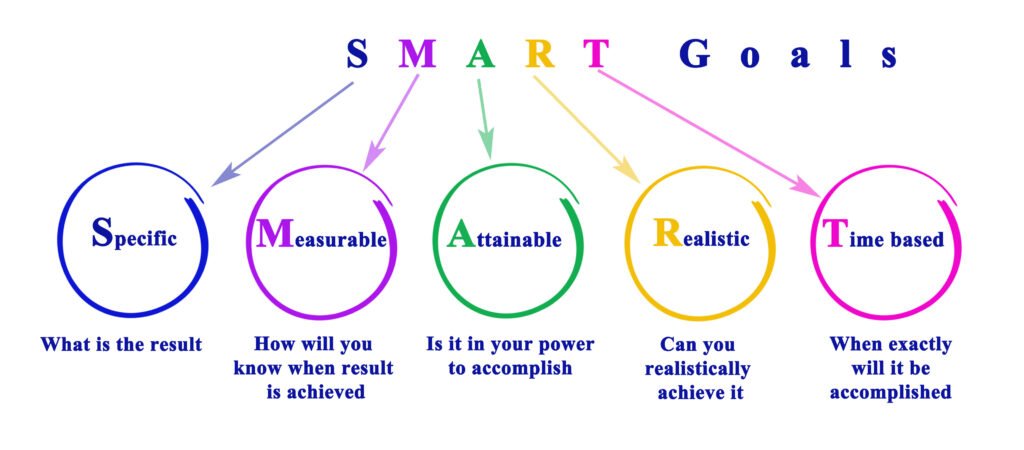

When setting financial goals, it’s important to consider both short-term and long-term objectives. Short-term goals may include saving for a down payment on a house or purchasing a new car, while long-term goals typically revolve around retirement planning. Setting specific, measurable, achievable, relevant, and time-bound (SMART) goals will provide clarity and help you stay motivated.

When it comes to investing, it’s important to educate yourself about different investment options. Stocks, bonds, mutual funds, and real estate are common investment vehicles that offer varying levels of risk and return. Consider consulting with a financial advisor or doing thorough research to determine the investment strategy that aligns with your goals and risk tolerance.

Maximize Tax Breaks

Understanding taxes is essential for effective personal finance management. Taxes impact our financial decisions and can significantly affect our overall financial well-being. Being knowledgeable about the different types of taxes and taking advantage of available deductions and credits can help optimize your tax situation.

Income tax is one of the most common types of taxes individuals encounter. It’s important to understand how tax brackets work and how different sources of income are taxed. Additionally, staying informed about changes in tax laws can help you make strategic financial decisions.

Maximizing tax deductions and credits is another way to optimize your tax situation. Deductions reduce your taxable income, while credits provide a dollar-for-dollar reduction in your tax liability. Common deductions and credits include mortgage interest, student loan interest, and education-related expenses. Researching and taking advantage of these opportunities can have a significant impact on your overall tax bill.

Retirement Planning

Retirement is a phase in life that we all look forward to, but to make it truly enjoyable, we need to plan ahead. The key to a secure and comfortable retirement lies in choosing the right retirement plan. Retirement corpus often requires long-term thinking and careful consideration. It’s never too early to start saving for retirement, as the power of compounding can significantly grow your savings over time.

There are many retirement savings vehicles available including 401(k) plan and Individual Retirement Accounts (IRAs) in United States, State Pension and Workplace pension in United Kingdom, Employee Provident Fund (EPF) and National Pension Scheme (NPS) in India . Many employers offer 401(k) plans/Workplace pension/EPF, which allow you to contribute a portion of your salary to a tax-advantaged retirement account. Some employers even match a percentage of your contributions, effectively doubling your savings. Individual Retirement Accounts (IRAs) are another option to consider, offering tax advantages and a wide range of investment options.

Understanding the different retirement savings options available to you in your respective region/country and determining the appropriate contribution amount based on your goals is crucial. Consult with a financial advisor or utilize online retirement calculators to estimate how much you’ll need to save to maintain your desired lifestyle during retirement.

Protect Your Money & Estate Planning

Protecting your financial future involves mitigating risks and ensuring that you and your loved ones are financially secure in the face of unexpected events. Insurance plays a vital role in safeguarding your assets and providing peace of mind.

Health insurance is essential to cover medical expenses and protect against high healthcare costs. Life insurance or Term Insurance is another important consideration, especially if you have dependents who rely on your income. Life or Term insurance provides a financial safety net for your loved ones in the event of your passing.

Additionally, property insurance can protect your home and belongings from damage or theft. It’s important to review your insurance policies regularly to ensure they adequately cover your assets and liabilities. Consulting with an insurance advisor can help you understand your coverage options and select the policies that best suit your needs.

Estate planning is another critical aspect of protecting your financial future. Creating a will ensures that your assets are distributed according to your wishes and minimizes potential conflicts among beneficiaries. Consider consulting with an attorney planner to guide you through the process and ensure your financial legacy is protected.

Monitor Your Credit Score

Regularly check your credit score to ensure it remains healthy. A good score is essential for obtaining favourable terms on loans and can save you money in the long run. Credit cards serve as the principal means by which your score is established and preserved. Therefore, the vigilance exercised in managing your credit spending corresponds directly to the oversight of your credit score. A robust credit history is imperative should you aspire to secure a lease, mortgage, or any form of financial assistance.

To facilitate bill payments, it is advisable to establish automated direct debits wherever feasible, thereby ensuring a consistent and punctual settlement of obligations. Subscribing to credit reporting agencies that furnish routine credit score updates is a prudent course of action. Furthermore, the vigilance to identify and rectify errors or instances of fraudulent activity is essential, and this can be accomplished through diligent monitoring of your credit report.

Financial Planning Process & Skills

The “Financial Planning Process” is a systematic approach to managing your finances, setting goals, and creating a plan to achieve those goals. It involves assessing your current financial situation, defining your objectives, and developing strategies to meet them.

Achieving financial stability hinges on harnessing existing skills, coupled with recognizing that the principles underpinning success in business and one’s career can seamlessly translate into effective personal financial management. Three pivotal proficiencies stand out:

1. Financial Prioritization: This involves the ability to scrutinize your financial landscape, identifying the sources that sustain your monetary inflow and ensuring unwavering dedication to these endeavours.

2. Cost-Benefit Analysis: This critical skill prevents overextension. Even the most ambitious individuals often harbour a plethora of ideas for potential lucrative ventures, be it a side business or an investment opportunity. However, treating your personal finances like a business mandates taking a step back to objectively evaluate the prospective costs and benefits before embarking on any new endeavour.

3. Spending Restraint: The ultimate cornerstone of successful financial management, akin to sound business practices, is the aptitude for controlling spending. Financial advisors frequently encounter high-earning individuals who paradoxically manage to outspend their earnings. After all, earning $250,000 a year proves futile if one dissipates $275,000 annually. Learning to curtail expenditures on non-wealth-enhancing assets until monthly savings or debt reduction targets are met remains pivotal in the journey to augmenting net worth.

4. The realm of personal finance: is abundant with guidelines and tips, each designed to steer individuals toward financial prudence. While these rules serve as valuable compass points, it’s crucial to remember that everyone’s financial circumstances are unique. Here are some rules that prudent individuals, particularly young adults, are advised not to break—though, under certain circumstances, deviation might be justified.

5. Saving or Investing – Set a Portion from Income: An optimal budget typically allocates a portion of one’s earnings for retirement savings, often in the range of 10% to 20%. However, it’s important to recognize that adhering strictly to this rule may not always be the wisest course, especially for young individuals who are just embarking on their financial journey. For many young adults and students, significant expenses like a new car, a home, or higher education loom large. Deducting 10% to 20% of available funds for retirement could significantly impede these crucial financial milestones. Furthermore, it may not be financially sensible to save for retirement when one is burdened with high-interest credit card debt or loans that erode potential gains. In such cases, the 19% interest on a Visa card, for instance, could easily offset any returns from a balanced mutual fund retirement portfolio. Ultimately, for young people who are still exploring their life path, saving money for travel and the experience of diverse cultures can be equally enriching.

- Long-term Investing and Managing Risks: Conventional wisdom suggests that young investors should adopt a long-term perspective and adhere to a buy-and-hold strategy. While this principle holds merit, there are justifiable reasons for departing from it, particularly when market conditions evolve. Adaptability can spell the difference between financial gains and mitigating losses. Short-term investing possesses its merits, regardless of age. Traditional investment theory recommends that young investors, given their extended investment horizon, should embrace higher-risk assets, as they have ample time to recover from potential losses. However, this doesn’t mandate taking undue risks with short- to medium-term investments. The concept of diversification plays a pivotal role in crafting a robust investment portfolio, encompassing the risk profile of individual assets and their intended investment horizon. Even as individuals approach retirement, there may still be room for some growth investments, especially considering that at age 60 or 65, they could have two or three more decades to navigate the financial landscape. Thus, the wisdom of incorporating growth investments remains a pertinent consideration.

Useful beginner friendly saving & investment strategies shall be used to be consistent in the saving and investment through out your life. Please make use of it.

Conclusion

Mastering personal finance is a lifelong journey that requires commitment, discipline, and continuous learning. By assessing your financial situation, creating a budget, managing debt, building a safety net during crisis/emergency, saving and investing wisely, understanding taxes, retirement planning, protecting your financial future, and continually improving your financial literacy, you can take control of your financial well-being and achieve your long-term goals. “Personal Finance Goals” in the financial planning process help you distinguish between good and bad financial decisions. By setting achievable objectives within your financial means, you focus on income and saving strategies to ensure wise financial choices.

Remember, personal finance is not a one-size-fits-all endeavour. Each individual’s circumstances and goals are unique, so it’s important to tailor your strategies and decisions to your specific needs. Take the information and tips provided in this guide as a starting point and adapt them to your own financial situation. With dedication and perseverance, you can master personal finance and pave the way for a financially secure future.

Frequently Asked Questions (FAQs)

Question: Who can benefit from mastering personal finance?

Answer: Anyone looking to take control of their financial future can benefit.

Question: What is the importance of mastering personal finance?

Answer: It helps you make informed decisions and achieve financial goals.

Question: What Are the 5 Main Components of Personal Finance?

Answer: The fundamental elements encompass income, expenditures, savings, investments, and safeguarding.

Question: How can one start mastering personal finance?

Answer: Start by assessing your current financials and tracking expenses, income and savings regularly. A fundamental principle is to ensure that your expenditures do not exceed your earnings. To illustrate, if your annual income is $10,000 but your annual spending totals $15,000, you will incur debt that accumulates over time, as you’ll be consistently spending beyond your means to cover past financial commitments.

Question: What if I have no financial background or knowledge?

Answer: No worries! There are plenty of resources, free online articles, financial services, educational materials, personal finance courses and courses on managing your money are available including our blog posts.

Question: How long does it take to master personal finance?

Answer: It varies, but with consistent effort, you can see progress within a few months. It’s a slow walk race which will assist in achieving personal financial goals.

Question: What if I’ve made mistakes in the past with my finances?

Answer: It’s never too late to start. Learn from past mistakes and focus on better habits going forward.